Market Intelligence, June 2026

Market size, country-level analysis, segmentation, key trends, major players, regulatory shifts, and analyst forecasts, all in one place.

Mordor Intelligence, CSIL, Market Data Forecast

$263B Market Value 2025

$358B Forecast 2031

5.26% CAGR 2026–2031

30%+ Global Market Share

The European furniture market is growing steadily, supported by renovation activity, hybrid work, tighter sustainability rules, and the continued rise of online retail.

Valued at USD 263.36 billion in 2025, the market is projected to exceed USD 358.26 billion by 2031.

This report covers market size, segmentation, country-level performance, key trends, major players, regulatory changes, and analyst expectations through 2031.

What are the European Furniture Markets?

Europe’s furniture industry covers home, office, contract, and hospitality segments across the continent’s major economies.

It is one of the largest furniture markets in the world, second only to Asia Pacific by volume, and is structurally shaped by a combination of consumer replacement cycles, commercial refurbishment demand, and increasing regulatory complexity around product sustainability.

The sector spans mass-market retail at one end and premium craftsmanship exports at the other, with countries like Germany, Italy, Poland, and the UK each playing distinct roles in production, consumption, and export.

How Europe Stands in the Global Furniture Industry

Europe accounts for over 30% of the global furniture market by value, making it one of the most significant demand and production regions in the world.

According to Fortune Business Insights, Europe accounted for 37.31% of the global luxury furniture segment in 2025, valued at USD 9.43 billion, with that figure expected to reach USD 9.91 billion in 2026.

China remains the top extra-EU supplier to the European market, followed by Türkiye and Vietnam, with import penetration from these corridors rising each year.

Italy and Germany maintain strong export positions within Europe and globally, supported by manufacturing quality and brand recognition.

European Furniture Market Size and Share

The European furniture industry holds a strong position in both current scale and long-term growth potential. Demand is consistent across residential, commercial, and hospitality segments, with the residential channel commanding the largest individual share.

Growth Trajectory 2026 to 2031

The market grows from USD 277.21 billion in 2026 to USD 358.26 billion by 2031 at a 5.26% compound annual growth rate. Europe accounts for over 30% of the global furniture market.

Home furniture commands more than 60% of total demand.

The mid-range price segment captured 48.64% of the European furniture market share in 2025, while online platforms are projected to grow at a 5.12% CAGR through 2031.

What is Driving the Market Forward

Growth is driven by renovation policy, hybrid work, sustainability rules, and demand for space-saving furniture.

The European Green Deal aims to double renovation rates by 2030 and to retrofit 35 million buildings, thereby supporting demand for replacement furniture.

Hybrid work is also lifting demand for ergonomic seating, adjustable desks, and storage.

According to the Mordor Intelligence Europe Furniture Market Report 2026, the European office furniture market is valued at USD 7.04 billion and is growing at a 6.5% CAGR from 2025 to 2030.

Sustainability regulation is also shifting competition.

The Mordor Intelligence Europe Sustainable Furniture Market forecasts the market to reach USD 18.01 billion by 2031. With 42% of Europeans aged 25 to 34 living in apartments under 60 square meters, demand for multifunctional furniture continues to build.

Market Segmentation by Application, Material, Price, and Channel

The European furniture industry is broken down into four primary axes: application, material, price range, and distribution channel. Each tells a different story about where demand sits today and where it is heading.

1. By Application: Home, Office, and Hospitality

Home furniture accounts for over 60% of total European furniture market demand, driven by residential renovations, urban housing growth, and replacement cycles averaging every five to seven years in the seating category.

Seating alone accounts for 38.5% of product share, underscoring the importance of sofas, armchairs, and office chairs across all settings.

Office furniture is the fastest-growing application segment, forecast to expand at a 6.72% CAGR through 2031.

Companies are redesigning spaces for hybrid work, and demand for compact, modular, and reconfigurable systems is rising sharply in both corporate and home-office settings.

2. By Material: Wood, Metal, and Polymers

Wood furniture holds the largest material share at 51.87% in 2025, underpinned by consumer preference, regulatory familiarity, and the established supply chains of major producing countries.

Plastics and polymers are the fastest-growing material category, set to expand at a 6.38% CAGR through 2031, driven by circular design mandates and cost advantages in volume production.

Metal remains a reliable material across contract and hospitality furniture, where fire safety compliance and durability are primary considerations.

3. By Price Range: Economy, Mid-Range, and Premium

Mid-range furniture dominated in 2025, capturing 48.64% of the European furniture market. Within the home furniture sub-segment specifically, mid-range accounted for 44.88% of consumer spend, reflecting consistent demand from households that prioritize quality without moving into luxury price bands.

Premium offerings are forecast to expand at a 5.83% CAGR through 2031, supported by affluent millennial household formation and rising interest in investment-grade furniture with verified sustainability credentials.

4. By Distribution: Retail, B2B, and Online

B2C retail channels accounted for 74.35% of the European furniture market in 2025 and are set to grow at a 7.33% CAGR through 2031, benefiting from continued investment in store networks by major players.

Online platforms are the fastest-growing distribution channel within home furniture, posting a 5.12% CAGR from 2026 to 2031.

The EU’s One-Stop-Shop VAT regime has made cross-border e-commerce structurally easier, particularly for mid-range sellers with scalable logistics.

| Segment | Leading Sub-Category | Market Share / CAGR | Outlook |

|---|---|---|---|

| Application | Home Furniture | 60%+ of total demand | Office fastest-growing: 6.72% CAGR |

| Material | Wood | 51.87% share (2025) | Polymers fastest: 6.38% CAGR |

| Price Range | Mid-Range | 48.64% share (2025) | Premium growing: 5.83% CAGR |

| Distribution | B2C Retail | 74.35% share (2025) | Online fastest: 5.12% CAGR |

Source: Mordor Intelligence; Europe Furniture Market Report (2026)

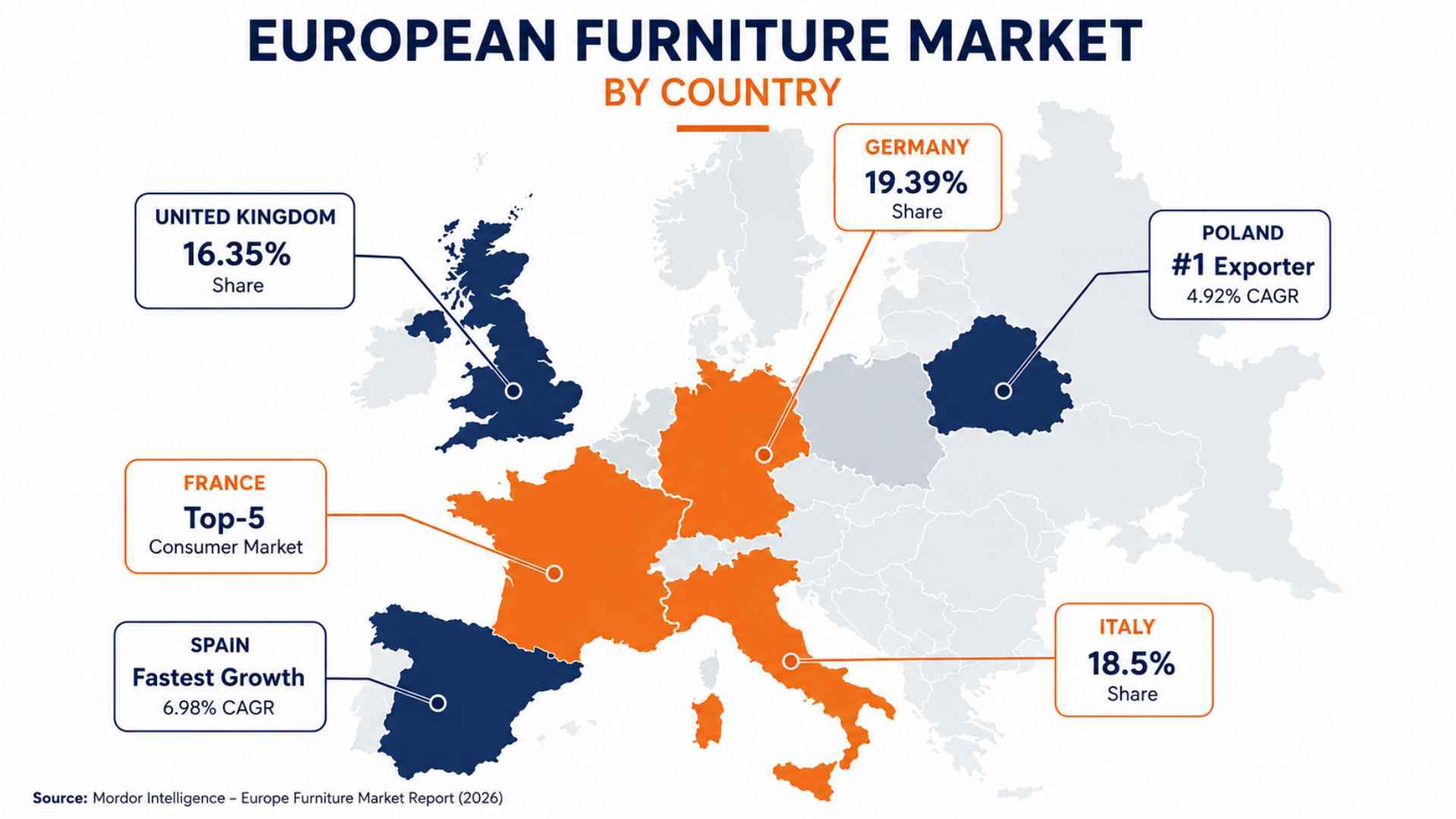

Geography and Country-Level Market Analysis

Growth and demand in the European furniture industry are far from evenly distributed.

Each country brings a different mix of manufacturing capacity, consumer spending habits, and export strength, making country-level performance an important factor in understanding the broader market.

Germany19.39% Market Share Germany held the largest share of the European home furniture market in 2025. |

Italy18.5% Market Share Italy was the leading furniture producer in Europe in 2025, generating EUR 26.7 billion in revenue and surpassing Germany. |

United Kingdom16.35% Market Share Together, Germany and the UK accounted for 35.74% of the European home furniture market in 2025. |

SpainFastest-Growing Market Spain is projected to grow at a 6.98% CAGR through 2031, the highest growth rate among major European furniture markets. |

PolandEurope’s Leading Furniture Exporter Poland is the largest furniture exporter in Europe by volume and produces approximately 50% of IKEA’s wooden furniture globally. |

FranceTop-Five Consumer Market France is among the five countries that account for nearly two-thirds of European furniture consumption. |

Europe’s furniture market is shaped by distinct national strengths, from Germany’s market leadership to Poland’s export power and Spain’s rapid growth.

Understanding these regional differences helps businesses identify opportunities, assess risks, and plan more effective market strategies.

Key Trends Reshaping the European Furniture Industry

Three forces are reshaping how furniture is made, sold, and bought across Europe: sustainability regulation, hybrid work, and e-commerce growth.

-

Sustainability and circular economy: ESPR, EUDR, and Digital Product Passports are making traceability, durability, repairability, and end-of-life data central to market access.

-

Hybrid work and home office growth: Office furniture is the fastest-growing application segment, with a 6.72% CAGR, as demand rises for modular, ergonomic, and adjustable products.

-

E-commerce expansion: Online channels are growing at 5.12% CAGR, supported by last-mile logistics, AR-enabled room planners, and easier cross-border sales through the EU OSS VAT regime.

These trends show that future growth will depend on compliance, flexible product design, and stronger digital retail capabilities.

Competitive Landscape and Brand Strategies

The European furniture industry is fragmented across thousands of manufacturers and retailers, but a smaller group of large players is increasingly shaping the market through consolidation, digital growth, and sustainability investment.

| Segment | Major Player | Strategy |

|---|---|---|

| Mass Market | IKEA Group | FY2025 total retail sales reached EUR 44.6 billion globally. Online sales accounted for 28% of all IKEA sales in 2025. |

| Mid-Premium Upholstery | Natuzzi S.p.A. | Competes in mid-to-premium upholstered furniture, with a strong export footprint across Western Europe. |

| Luxury Contract | Poltrona Frau Group | Focuses on craftsmanship-led seating across luxury residential and hospitality projects. |

| Commercial Office | Steelcase | Advancing circular credentials through life-cycle assessments and Cradle to Cradle certification. |

| Volume Retail | XXXLutz Group | Finalized the acquisition of Porta Group in January 2025, adding 140 stores across Germany, the Czech Republic, and Slovakia. |

| Luxury / Editorial | Roche Bobois | Competes through design exclusivity, limited-run collections, and strong positioning in high-end residential interiors. |

How Leading Brands Are Staying Ahead

IKEA invested more than EUR 2.1 billion in price reductions in FY2024, helping drive store visitation up by 3% and online orders up 9%.

In FY2025, online sales represented 28% of total retail sales, while Ingka Group reported EUR 41.5 billion in revenue, with store visits up 1.3% and online visits up 4.6%.

Herman Miller debuted bamboo upholstery for its Eames Lounge Chair in July 2024, cutting environmental impact by 35%. Steelcase and Vitra are leading in low-carbon product lines with verified sustainability claims that meet rising corporate ESG standards. B&B Italia partnered with Luminaire to open a flagship showroom in the Los Angeles Design District in March 2026.

Sources: Ingka Group IKEA FY2024 Annual Summary , IKEA Global FY2025 Retail Sales.

Regulatory Timeline: What the Industry Must Prepare For

Europe’s furniture rules are tightening quickly, with ESPR, EUDR, Digital Product Passports, and renovation targets shaping compliance through 2031.

-

2024 ESPR enters into force: The Ecodesign for Sustainable Products Regulation entered into force in July 2024, replacing the previous Ecodesign Directive and extending its scope to physical products, including furniture.

-

2026 EUDR deadline: Large furniture brands must prove that wood-based materials are deforestation-free and fully traceable by December 2026. The ESPR DPP registry is also scheduled to launch by July 2026 for the first priority product groups.

-

2028 furniture-specific rules expected: ESPR delegated acts for furniture are expected around 2028. Once adopted, companies will have 18 months to implement Digital Product Passports covering material composition, environmental performance, repairability, and end-of-life guidance.

-

2030+ renovation wave target: The European Green Deal targets 35 million building retrofits and aims to double renovation rates by 2030, creating long-term furniture demand across the decade.

These milestones show that furniture brands must prepare early for traceability, product documentation, circular design, and renovation-linked demand.

Sources: ASUENE EU DPP Complete Compliance Guide, Circularise DPP EU Legislation Timeline , Complir ESPR Regulation Explained.

Expert Views and Analyst Forecasts 2026–2031

Leading research firms are broadly aligned on the direction of the European furniture industry through 2031, though short-term demand signals call for measured optimism.

“The growth outlook reflects persistent tailwinds from EU renovation programs, hybrid work normalization, and demographic demand for ergonomic solutions.”

Mordor Intelligence, Europe Furniture Market Report 2026

Mordor Intelligence projects the market will reach USD 358.26 billion by 2031 at a 5.26% CAGR, with Spain as the fastest-growing country market and office furniture as the fastest-growing application. The firm also confirms that sustainability has shifted from a differentiator to a structural requirement.

CSIL takes a more cautious near-term view, noting that European furniture demand is expected to stay nearly flat in 2026 as households spend cautiously amid uncertainty and a shift in discretionary budgets toward experiences over durable goods.

Market Data Forecast projects USD 409.92 billion by 2034 at a 4.95% CAGR, reflecting a steady structural growth path rather than a cyclical bounce.

What the Data Tells You About the Road Ahead

The European furniture market remains structurally strong, with growth through 2031 supported by renovation policy, hybrid work, demographic shifts, and demand for sustainable, space-efficient design.

Still, 2026 may be a slower year as households spend cautiously.

Brands that invest early in circularity compliance, digital retail, product documentation, traceability, and repairability will be better prepared for EUDR deadlines, future ESPR rules, and Digital Product Passports.

For businesses planning their next move, now is the time to prepare before compliance pressure and competition intensify.

European Furniture Markets Report, Data updated June 2026. This report is for informational purposes only. Market projections come from third-party research firms and may change over time. Primary sources include Mordor Intelligence , Market Data Forecast , CSIL , Ingka Group , IKEA , ASUENE , Circularise , and Complir .

Frequently Asked Questions

How Important is Online Retail to The European Furniture Market?

Online retail is becoming increasingly important as consumers expect convenient shopping, faster delivery, virtual room-planning tools, and a broader product selection.

Which Furniture Segment is Growing The Fastest In Europe?

Office furniture is currently the fastest-growing application segment, driven by hybrid work trends and demand for ergonomic, adaptable workplace solutions.

Why is Sustainability Becoming a Competitive Advantage for Furniture Brands?

Consumers, regulators, and corporate buyers increasingly favor products with strong environmental credentials, encouraging investment in circular design and traceable supply chains.

How Does The EU Renovation Wave Affect Furniture Demand?

The EU’s renovation targets are expected to increase replacement and refurbishment activity, creating long-term demand across residential, commercial, and hospitality furniture segments.