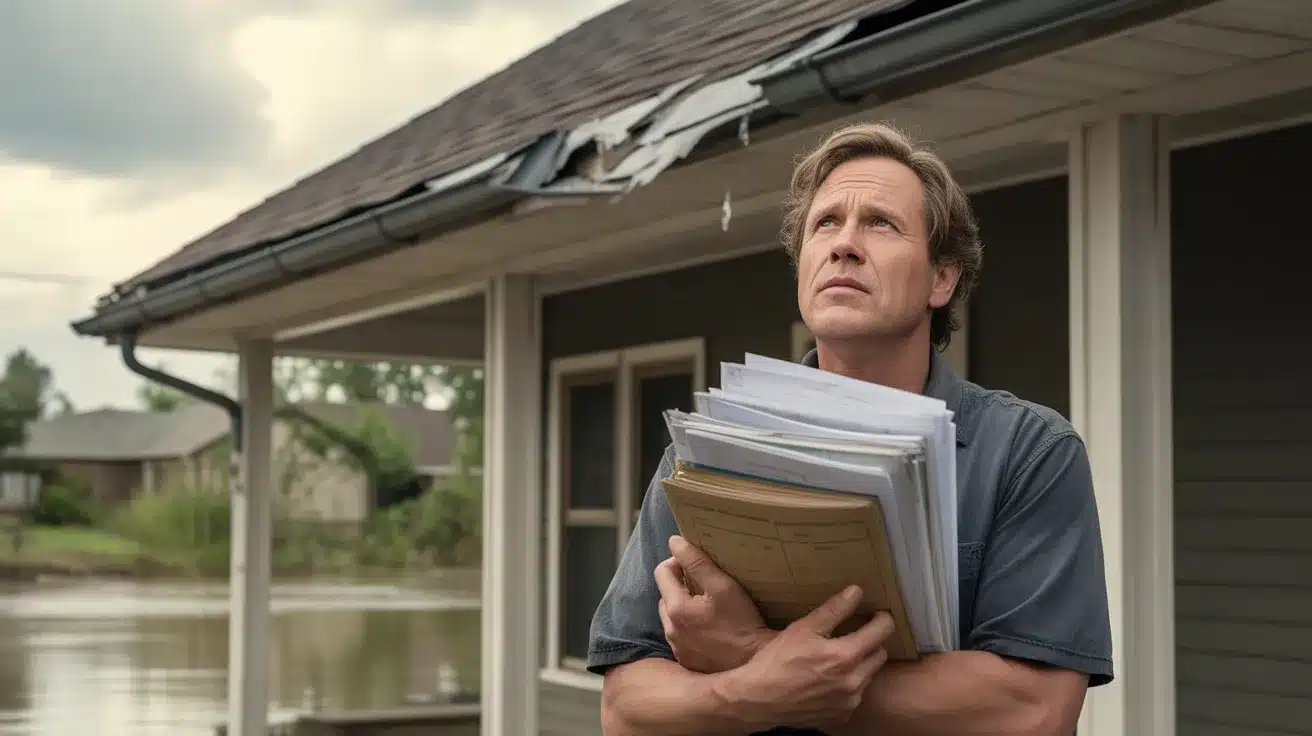

You did everything right: called your insurance company, filed your claim, and waited patiently. Then came the shocker: your roof claim was denied. Now what?

A denied claim can feel like a punch to the gut, especially when your roof is damaged and time isn’t on your side. But don’t panic, you have options, and this isn’t the end of the road.

With the right steps, you can challenge the decision, gather stronger evidence, and even reverse it.

In this guide, we’ll break it down in plain English, just smart, actionable steps to get you back on track. If it’s appealing the denial or preventing it next time, we’ve got you covered from shingle to settlement.

Why Was My Roof Claim Denied?

Getting denied for a roof claim can feel confusing and unfair, but most insurance companies follow specific guidelines.

Understanding why your claim was rejected is the first step in taking control of the situation.

Normal Wear and Tear

Insurance is meant to protect against sudden, accidental damage, not the natural aging process.

If your roof is 15–20 years old and showing signs of deterioration, such as cracked shingles, missing granules, or brittle edges, insurers may classify it as “wear and tear.”

Even if a recent storm made things worse, they might argue that the roof was already too worn out to qualify. In these cases, full replacements are often denied, and they may offer a partial payout or nothing at all.

Lack of Maintenance

Let’s say your gutters have been overflowing for months, or there’s visible moss growth and signs of leakage. Insurance companies will see these as red flags. They expect homeowners to care for their property regularly.

If damage appears to have built up over time, like rotting wood, sagging areas, or mold, they may say it could have been prevented with proper upkeep. Unfortunately, that’s grounds for denial under most policies.

Policy Exclusions

Every policy has fine print, and that’s where many denials begin. Some insurance plans exclude certain types of roof damage altogether, especially if it’s caused by:

-

Earthquakes

-

Flooding

-

Poor construction

-

Manufacturer defects

Others may only cover specific materials or have strict limits based on your roof’s age. If your claim falls into one of these “exclusion zones,” it may be denied even if the damage looks severe.

What to Do If You Can’t Afford Roof Repairs After a Denied Claim

Sometimes, a denied claim leaves you with no payout and a roof that still needs fixing. If you’re facing high repair costs, here are a few practical options:

-

Ask your roofing contractor about payment plans: Many roofing companies offer financing options or staged payments to help you spread out the cost.

-

Look into home improvement loans or grants: FHA Title I loans, personal loans, or local assistance programs may be available, especially if you’re a senior, veteran, or low-income homeowner.

-

Use a credit card as a last resort: If you’re in a bind, a low-interest credit card might help with urgent repairs. Just be sure to budget for repayment.

-

Crowdfund or ask for community support: In urgent cases, reaching out to friends, family, or even local non-profits can sometimes bridge the gap.

Step-by-Step Guide to Appealing a Denied Roof Claim

A denied roof claim doesn’t always mean the end of the road. If you believe your denial was unfair or incorrect, you have every right to push back. Here’s a clear, step-by-step guide to help you confidently appeal the decision:

Step 1: Carefully Read the Denial Letter and Policy Terms

Start by reading the denial letter from your insurance company. Look for:

-

The specific reason(s) your claim was denied

-

Any policy clauses they refer to

-

Deadlines for appealing

This will help you determine whether the issue was a misunderstanding, a technicality, or something more serious.

Step 2: Document the Damage with Photos and Inspection Reports

Strong evidence is key. Take clear, high-resolution photos of:

-

All visible roof damage

-

Water stains or leaks inside the home

-

Damaged gutters or shingles

This professional documentation will support your claim and prove the damage is storm-related or sudden, not due to neglect or age.

Step 3: Contact a Roofing Contractor or Public Adjuster

Bring in an expert to give a second opinion. A licensed roofing contractor can:

-

Assess the true cause and extent of damage

-

Spot issues the insurance adjuster may have missed

-

Provide an estimate for repair or replacement

Alternatively, a public adjuster works on your behalf to re-evaluate the claim and help you gather a stronger case.

Step 4: File an Appeal with Supporting Evidence

Once you’ve gathered enough proof, submit a formal appeal. Include:

-

A cover letter explaining why you believe the denial was wrong

-

Photos and videos of the damage

-

The roofing inspection report

-

Any written statements from contractors or adjusters

Be sure to send this before the deadline listed in your denial letter. Keep copies of everything you submit and note the date it was sent.

When to Involve a Lawyer or State Insurance Department

If your appeal gets denied again or you’re being ignored, it may be time to escalate:

-

Hire a lawyer who specializes in insurance disputes. They can negotiate directly or take legal action if needed.

-

Contact your state’s insurance department to file a complaint. They can investigate if your insurer is acting unfairly.

How to Prevent Future Roof Claim Issues

Avoiding claim denials starts with being proactive. Here are smart steps you can take to strengthen your case before damage ever happens:

-

Schedule regular roof inspections: Get your roof checked by a professional once a year, or after major storms, to catch small issues early.

-

Keep photo records of your roof’s condition: Take clear pictures of your roof in good shape. These can be valuable proof if you ever need to show the “before” condition.

-

Clean gutters and downspouts regularly: Clogged gutters can lead to water buildup and damage. Clean them seasonally to prevent problems.

-

Make timely repairs: Fix minor leaks, missing shingles, or flashing issues immediately. Ignoring small problems can make insurers deny future claims.

-

Review and update your policy: Make sure your roof is fully covered, especially if it’s older or made from specialty materials. Talk to your agent to fill any coverage gaps.

-

Keep a file of receipts and inspection reports: Having documentation of past maintenance and professional assessments can strengthen your claim and show you’re a responsible homeowner.

Conclusion

Getting your roof claim denied can feel frustrating, but it doesn’t have to be the end of the road.

By understanding the reasons behind the denial and taking proactive steps, from gathering evidence to filing an appeal, you can make a strong case to reverse the decision.

Even if the outcome doesn’t change, there are still effective strategies for managing repair costs and protecting your home in the future.

Please drop your tips or questions in the comments below. We’d really like to hear your experience and help others in similar situations.